Some Central Banks have begun to analyze the potential of issuing their own digital coins, and as we told in previous articles, they are getting closer to doing so.

But beyond the news, or rumors, it is good to know more about what we are talking about when we talk about CBDC or Central Bank Digital Currency.

In this brief article we will ask ourselves things like What is a CBDC, what are the characteristics of a CBDC, or How do CBDCs work, among other interesting facts.

What is a Digital Currency from a Central Bank or CBDC?

CBDC stands for Central Bank Digital Currency. This currency is a way of issuing digital trust money by a central bank, for a given nation and in a given territory.

In a way, the strategy behind this is to give a new face to the trust money we all know but adding some characteristics that crypt coins have.

We say “some” because clearly a money commanded by a central bank lacks the basic benefits of a crypto currency with respect to privacy and decentralization.

It is worth clarifying that the CBDCs are not crypto-currencies like Bitcoin, Ethereum, etc. but a simple reaction of governments and banks to the growth and “threat” of crypto-currencies.

Why are the banks and governments concerned? Because they are losing economic and financial power in the hands of free currencies that compete against the monopoly of money executed by the central banks in each country.

The access to information, enhanced by the Internet, increasingly reveals this shameless monopoly that has led many countries to ruin, as we have already told you in articles such as: Argentina and bitcoin as a refuge.

Objectives of the CBDC

Aware that their business is in decline, governments are pushing for a form of money that will help them achieve different economic, political, geo-economic and geopolitical goals and where spying on the population will reach levels never seen before.

Among those cases, we have already reviewed China’s proposals with the electronic Renminbi or the European Union’s with the Euro Digital. Although the differences in objectives vary from one state to another, in general the reasons for implementing a CBDC are:

– To create a new form of money that can take advantage of all the technology that has been developed by the crypto-currencies up to this moment.

– To promote new monetary and financial structures that encourage investment by nations and the world.

– To improve and simplify national and international trade.

– Stimulate competition between various payment systems, making them more economical and improving their reach.

– Develop mechanisms for rapid and immediate control over monetary policy.

– Create a control structure that allows us to know what the course of money is from the origin to the end at all times.

– Replace the anonymity of money with control by the entities that control CBDCs.

How do CBDCs work?

The way a CBDC works depends on the technology and the purposes for which the currency was created. Just like cryptosystems, each can have a different technology and function. In this case, it will depend on the interests of the Central Bank that issues it.

As we have seen, many of these Central Banks have set their eyes on blockchain technology and distributed accounting books. The reason is that this technology facilitates the creation of systems that are interoperable with other currencies, as we see with crypto-currencies today.

Also, CBDCs could have the possibility of implementing technologies such as smart contracts, unthinkable in today’s trust money.

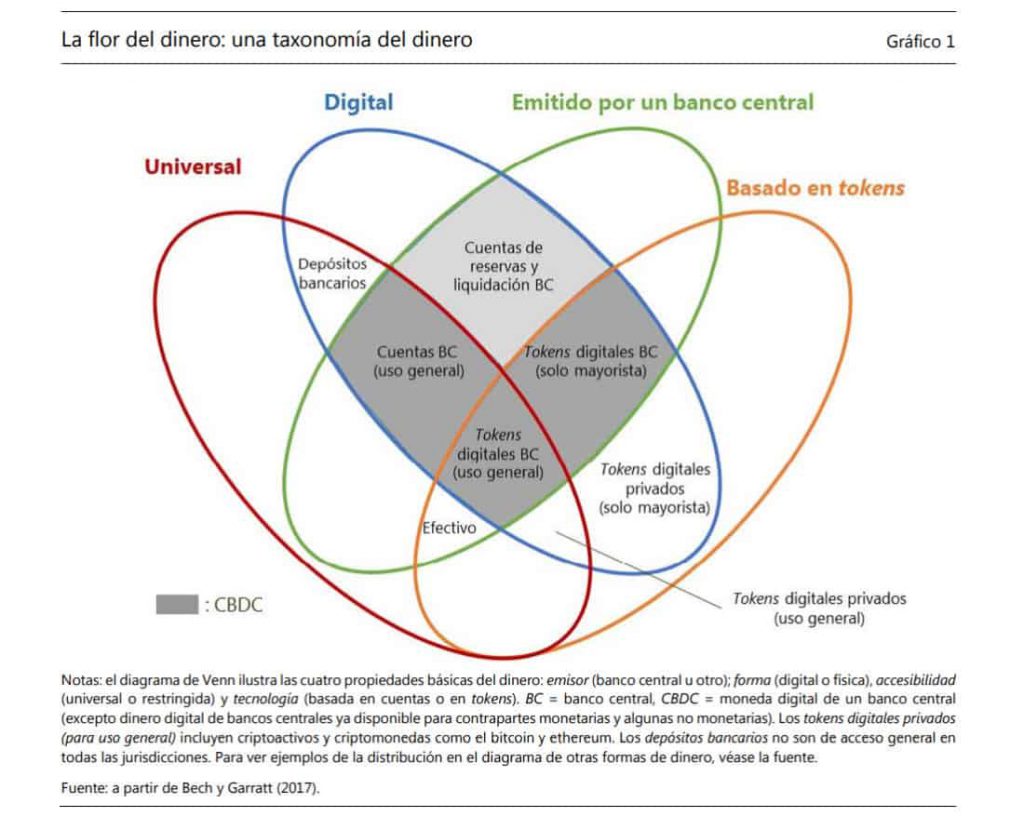

CBDC operating models

In the image above we can see different functioning of the CBDC depending on the objectives pursued by that currency.

1- To improve the operation of the wholesale payment systems.

2- Substitute cash for a more efficient alternative

3- Improve available monetary policy instruments, especially when faced with the lower limit of zero

4- Reduce the frequency and cost of banking crises.

Each one of them generates (in gray colors) different areas where the CBDC are possible, each one of them with its own characteristics.

Whatever the case may be, it is clear that the objectives that the Banks and the State set themselves will define the way in which a CBDC will work and what its characteristics will be at certain times.

Differences between CBDCs and Bitcoin

To help you understand the main differences between having a CBDC and buying bitcoin we will make a brief comparison:

Monetary Policy

– In Bitcoin only 21M of Bitcoin will be created and this cannot be changed.

– In the CBDCs this will remain in the hands of the issuing entity so they will certainly be susceptible to inflation.

Geography

– BTC is accessible to everyone without limits of borders.

– A BTC will be limited to the territory determined by the issuing government.

Storage

– At Bitcoin, anyone can receive and save Bitcoins with their own security seed.

– In a CBDC, users can be exposed to censorship if they don’t comply with the requirements.

Transfer

– At BTC anyone can transfer value as long as they have the internet and their private key.

– In Central Bank Currencies it will depend on the requirements imposed by the central banks.

The synthesis of the creation of the CBDCs can be summarized in the phrase “Barran Sancho, signal that we ride“.

The Central Banks will try to coercively limit the use of the crypto-currencies by imposing (as they can) the use of their own digital form of currency.

Will they be able to stop or pause the advance of the crypto coins? My personal opinion is that they have no chance.